Mixed Credit Reports

The credit reporting agencies collect information about you and store it in their databases. Equifax, Experian, and Trans Union all have their own database. This is why you have three different credit reports. The databases contain hundreds of millions of bits of raw data, referred to as credit files. Most consumers have more than one credit file. Credit files are used to generate credit reports. A mixed credit report is the result of a credit reporting agency’s inaccurate merging of credit information and/or an entire credit file belonging to one consumer into the credit report of another consumer.

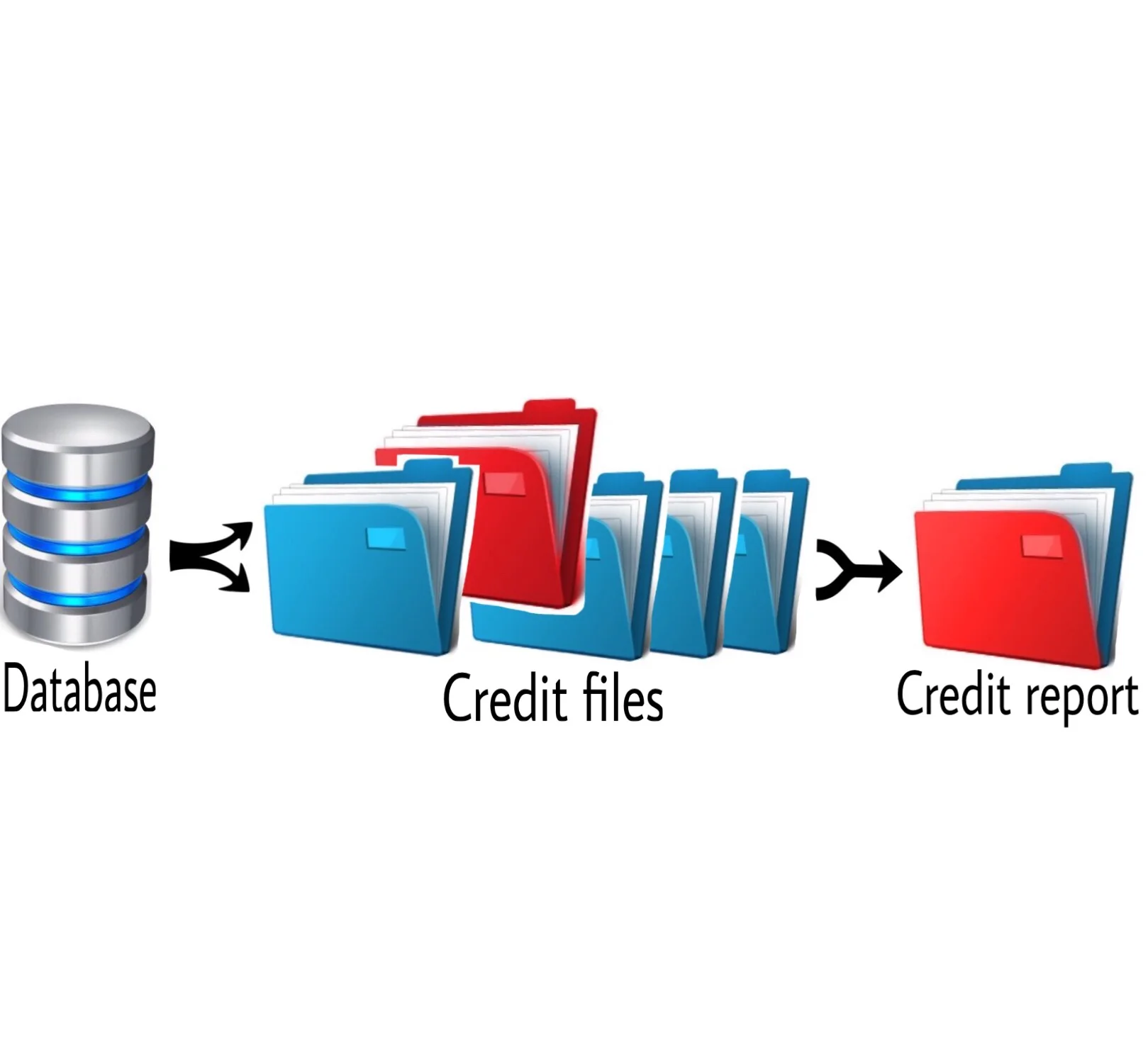

When your credit history is requested, the credit reporting agencies sort though the millions of bits of electronic data stored within their databases. Search results defer depending upon the search terms used. For example: the results of a search for Jane Doe may vary from the results for a search for Jane A. Doe. The searches pull the credit files assumed to be yours, and merges all of the credit files in to a credit report.

Using the image below, imagine that all of the blue credit files are yours. The red credit file belongs to someone who has the exact same name as you. In this instance, the databases algorithms (the database rules) inadvertently merges the other person's credit file with yours. As a result, you have a mixed credit report.

Why do mixed credit reports happen?

There are many possible causes for the merging of credit files, but all of them relate in one way or another to the algorithms used by the consumer reporting agencies. A mixed credit report could be caused by an improper algorithm just as it could be caused by the inaccurate reporting of a consumer's personal information.

Why so many credit files?

Numerous credit files may exist on a single consumer for the following reasons:

- Consumer reporting agencies may not have enough information to say with the highest degree of certainty that each of the credit files should "merge."

- The various creditors' records do not always identify an individual consumer in the same way. (One way may be by first and last name, and the other way would be by first, middle, and last name).

- Consumers may use two or more names in their credit activities (such as nick names, maiden and married names, names with and without generational suffixes).

- Consumers may have two or more addresses (such as home/school, work/home or vacation or second homes).

- Creditor's records may misspell or invert letters in names, street addresses, or social security numbers.

Even though federal law requires credit reporting agencies to disclose any and all information relating to an individual consumer, numerous credit files often results in incomplete reporting. Incompleteness is not the only concern consumers should have. Take into account that there are many inaccuracies contained within the credit reporting agencies databases, and the more files to sort through and match increases in likeliness of inaccurate information being reported.

What to do if you have a mixed credit report?

If you suspect your credit report contains information belonging to someone else, dispute the information right away. For sample complaint letters and step-by-step instructions on how to dispute your credit report, click here.